Second article: Life insurance, a "legal scam

To find out which is the best possible investment, the author reviews seven alternatives. After the first article on the uncertain nature of property, here is the second on life insurance.

Second article: Life insurance, a "legal scam

In 1983, the Hamburg District Court (74 047/83) ruled that life insurance was a "legal swindle" (legaler Betrug). This severe ruling was fully justified, then as now.

Life insurance is a savings contract with an insurer or bank, which undertakes to pay out the capital plus a capital gain at the end of the contract. If the policyholder dies before the end of the contract, the sum due is paid to the beneficiaries designated when the policy was taken out.

The specific terms and conditions (contribution, term, type of investment, charges, taxation, etc.) vary from contract to contract, company to company and country to country. Here are a few concrete cases, by way of representative samples.

To promote their product, insurers point to a number of tax advantages, including the fact that contributions can be deducted from income, or that after a certain period of time, capital gains are not taxable. But these advantages are limited by fairly low ceilings. In France, for example, gains after eight years are tax-free up to €4,600 (€9,200 for a couple), but taxed at 7.5% above that figure. Not forgetting the annual social security deductions of 15.5% on interest.

To promote their product, insurers point to a number of tax advantages, including the fact that contributions can be deducted from income, or that after a certain period of time, capital gains are not taxable. But these advantages are limited by fairly low ceilings. In France, for example, gains after eight years are tax-free up to €4,600 (€9,200 for a couple), but taxed at 7.5% above that figure. Not forgetting the annual social security deductions of 15.5% on interest.

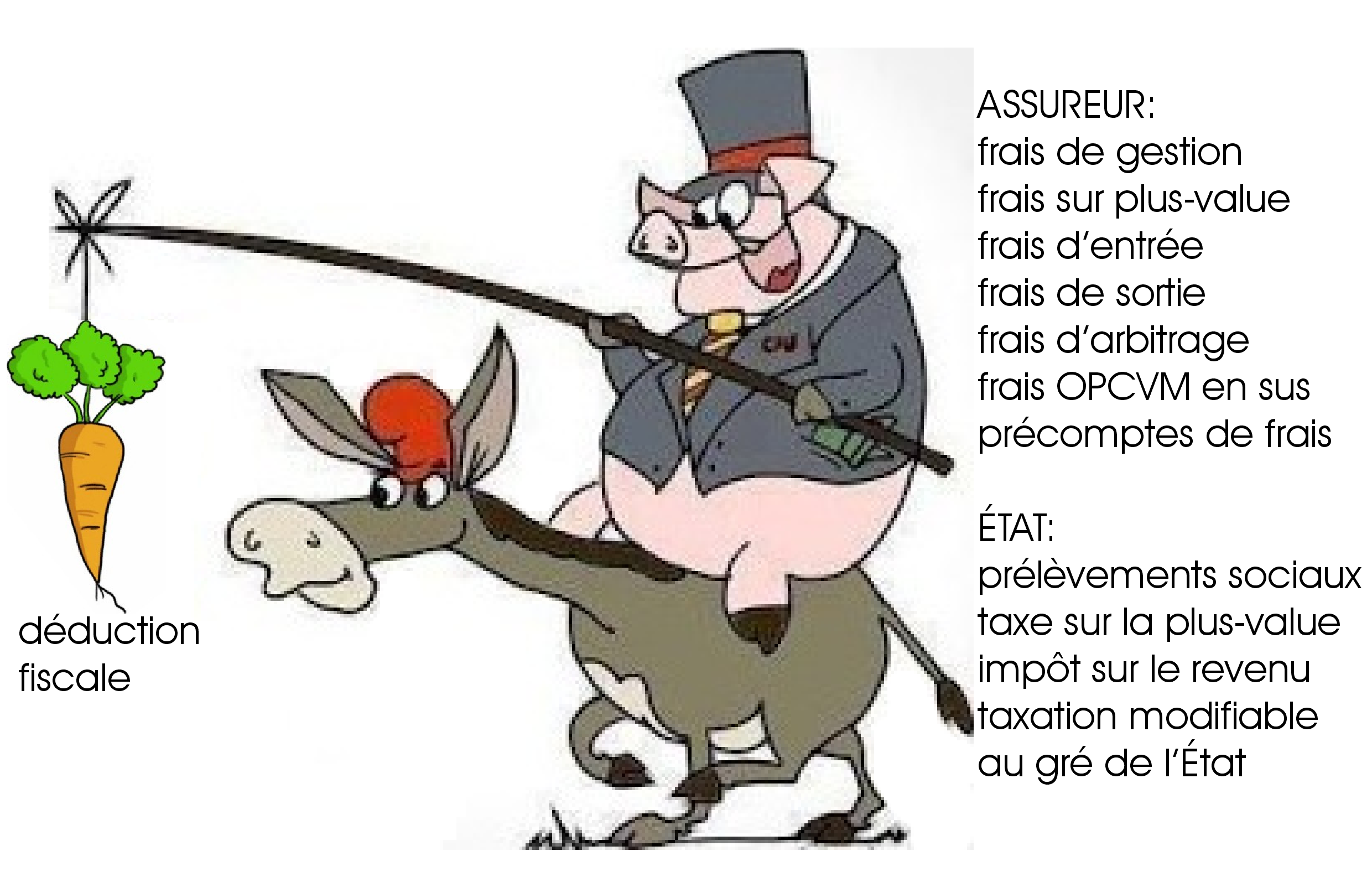

So there are a few tax advantages, but they are limited, debatable and have an uncertain future, given that the legislator can change the taxation rules at will. These tax breaks are the only argument, more or less valid, in favour of life assurance. But this tempting tax regime is more a carrot to lure investors. Because this product is essentially designed to maximise the insurer's profits, to the detriment of the policyholder.

I know someone who took out several life insurance policies with Crédit Mutuel, with a 'conservative' profile to avoid risky investments. After several years, he got scared by the collapse of Lehman Brothers and closed his policies. The bank reimbursed him less than the amount of the contributions he had paid in. What's the point of tax-free profits if the investment ends in a loss?

This is just one case among millions. The disastrous cases where policyholders are reimbursed less than their contributions (not to mention inflation, which reduces the purchasing power of their capital through currency erosion) are commonplace, because the insurer 1° charges management fees and 2° mismanages the sums entrusted to it.

Costs that eat into profitability

Companies charge annual management fees (a variable percentage of the capital). They may also charge capital gains fees (variable percentage), entry fees (for each payment, you are charged an average of between 3 and 5%), and sometimes even exit fees. For multi-support contracts, you will still have to pay arbitration fees and, if the life insurance invests in a Undertaking for Collective Investment in Transferable Securities (SICAV and mutual funds), the policyholder will have to pay additional fees, as the UCITS charge their own fees on top.

Pre-authorised deduction of charges means that the charges are not spread over the life of the contract, but are deducted at the beginning. It will then take a good number of years for this initial loss to be made up by the interest earned on the savings. "All your payments in the first few years are deducted as charges! Absolutely nothing goes into your savings. To see this, look at the table of surrender values. [For retirement savings offered by the French insurer GAN], surrender before 18 months is 0! Yes, you've got it right, the first 18 contributions of 150 euros went entirely into their pockets...

Pre-authorised deduction of charges means that the charges are not spread over the life of the contract, but are deducted at the beginning. It will then take a good number of years for this initial loss to be made up by the interest earned on the savings. "All your payments in the first few years are deducted as charges! Absolutely nothing goes into your savings. To see this, look at the table of surrender values. [For retirement savings offered by the French insurer GAN], surrender before 18 months is 0! Yes, you've got it right, the first 18 contributions of 150 euros went entirely into their pockets...

And it doesn't stop there. The percentage of the surrender value gradually increases, reaching a painful 100% after 10 years. Clearly, if for any reason you were to withdraw your investment before 10 years, you would be out of pocket. [...]

Under life insurance legislation, capital gains after 8 years are no longer taxed (up to a certain limit). However, with these rotten contracts, even between 8 and 10 years, you lose money. In practical terms, if you cancel your policy, you will get back less than you paid in premiums" (http://forum.actufinance.fr/assurance-vie-les-arnaques-eviter-P197505/).

The mechanism of early deduction of costs is ingenious, because it discourages those who would like to get out of this mess before the contract expires. I have a German friend who would like to cancel his life insurance policy, but he won't because he would lose 30% of the money invested - not to mention the loss of purchasing power due to inflation!

"AXA, the world's leading insurance brand, has published its results for 2011. In the "life, savings and pensions" branch, with premium income of €52,431m, AXA collected fees of €2,267m, or 4.3% per annum from customers.

AXA is particularly hard on new savings customers: "new business volume €5,733m, new business margin 25.2%" (www.axa.com). A quarter of your savings parasitized by the insurer!

Allianz, one of the world's largest insurance companies, reveals that its commissions and services earned it €8406m in 2011; if we deduct the €1087m relating to property and casualty insurance, the free riding of life insurance and investment managers at Allianz costs savers more than €7bn a year (2011 annual report, p. 295, www.allianz.com).

In Germany, the State grants tax deductions to those who contribute to supplementary pensions ("Riester" or "Rürup"). 15% of savings disappear into the pockets of insurers, and you have to reach the age of 85, or even 92, for the investment to finally earn more than it cost the subscriber.

As you can see, motivated by the carrot of tax deductions, the donkey moves forward with all its might, pulling the life insurance wagon behind it, to the great profit of the insurer or bank that sold it this juicy contract.

Pitiful management

Life insurance policyholders' money is invested either in money market funds (bonds) or in the stock market (shares). In both cases, there's nothing to be proud of:

The average return on euro funds fell from 5.3% in 2000 to 3% in 2011 (Capital. Guide des placements 2013, p. 18). But since 2000, the eurozone's M3 money supply has doubled, which, after deducting GDP growth, gives inflation of around 8% a year (much higher than the 2% of misleading government statistics). Since the interest rate on the funds is lower than the rate of inflation, the return is negative. Anyone who invests their savings in a euro-denominated life insurance policy loses around 4 to 5% of their purchasing power every year.

The stock market crash in autumn 2008 showed that equity portfolio managers are poor decision-makers. None of them anticipated the collapse, and all of them drank the cup.

As a result, whether life insurance money is invested in the currency market (money market funds) or on the stock market (equity portfolios), management is pathetic.

Hidden risks

As everyone knows that the stock market rises and falls, the policyholder of a life insurance policy based on shares is more or less aware of this risk.

On the other hand, if the life insurance is based on currencies, the policyholder generally has no idea of the underlying risks. Most brave policyholders are completely unaware of the risks inherent in money market funds, which invest in shaky government bonds, reckless corporate 'subordinated debt' and risky derivatives.

Government bonds are not at all a sensible investment. Let's not talk about Greece, which everyone knows is on life support. Let's take the case of a major economic power, France, instead. On 21 September 2007, Prime Minister François Fillon declared: "I am at the head of a State that is financially bankrupt, I am at the head of a State that has had a chronic deficit for 15 years, I am at the head of a State that has never voted for a balanced budget in 25 years. "If France were a company, a household, it would be in suspension of payments". Since Fillon's statement, the default has been postponed, quite simply by borrowing even more. Interest payments to creditors are financed by new borrowing. It's as if a household unable to pay its mortgages took out revolving credit to delay foreclosure. Between 2007 and 2012, French government debt increased by €500 billion! On 27 January 2013 on Radio J, Labour Minister Michel Sapin confirmed that France is "a totally bankrupt state".

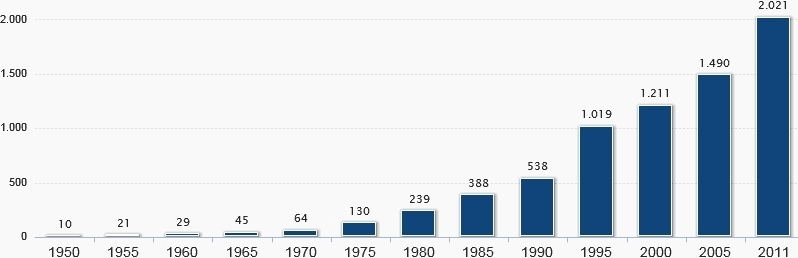

Germany, which is always held up as an example of success, is hardly better off. It too is widening its budget deficit and its national debt every year. Interest payments on the current debt are financed by additional borrowing (Neuverschuldung).

German debt (State, regions, municipalities) from 1950 to 2011 in billions of euros

Germany's debt has been growing steadily for decades, and the pace is accelerating over time as a result of compound interest. The exponential curve will rise faster and higher every year, until the predictable and inevitable default.

If your life insurance savings have been used to acquire post-deposited company loans, that's not reassuring either. Some insurers are crazy about paper whose yield is admittedly slightly higher than average, but whose reliability is dubious: "postponed loans", where the company's creditor agrees to his claim being placed at a lower rank than that of all the company's other claims. In the event of the company's bankruptcy, it will be paid last, if there is anything left over after all the other creditors have been repaid.

Postponed bank loans have been acquired on a massive scale by life insurers. The Spanish giant Bankia, ruined by the property crisis, no longer has any equity capital; it is even said to have "negative capital". The world's other major banks have plenty of toxic assets (worthless, or impossible to value) on their balance sheets. Wouldn't it be foolhardy to buy a subordinated loan from a bank for which you will be the last creditor to be served?

Bank run! The holder of the postponed claim will be served after everyone else!

Finally, derivatives are highly speculative. An investment broker, whose clients included major companies such as Allianz, recounts: "In the past, all life insurers bought thirty-year IOUs from companies, which were not very profitable, but safe. For the past 5 or 6 years, my brokerage business has been getting worse and worse, because these insurers now only buy [...] pure bets. If such and such an event occurs with a 50% probability, then we extrapolate over 30 years for each year. How many question marks remain? Hundreds; who knows if the equation will allow us to land on our feet. But we did. Almost all life insurers now only have long-term bets in their inventory" ("Ein Versicherer packt aus", 1.2.2009, www.mmnews.de).

These bets are worth nothing now. They are so complex that it is impossible to calculate their current value. Unsaleable. The broker gives as an example a structure that was sold to an insurer in 2006, but was completely unsaleable from 2009: "2 years of interest at 4% until 25.5.2008, then factor 5.4 times (30 years swap minus 2 years swap), minimum 0%, maximum 7%, maturity 25.5.2020. With an inverted interest rate structure - as we have had for some time - this thing blows up in your face. So 0% interest. Well, you might say now, at least the capital invested will remain. But here Lehman was very often the issuer, and therefore worthless.

Even if it were Goldman Sachs or Merrill Lynch, no bank in the world sets a redemption price for [this type of paper] any more. In other words, the insurer has 0% paper in its inventory until 25.5.2020, probably worth between €30 million and €50 million [...], and this paper cannot be sold until then".

There has been a lot of talk about the possibility of a banking crash, but few people see the danger of a life insurance crash! And yet the risk is very real: insurers hold shares, the price of which depends on the stock market (which will fall as the economic crisis worsens) and bad debts - government bonds, subordinated loans, derivatives. Did you know that the insurers' guarantee fund is ridiculously tiny, absolutely insufficient to reimburse policyholders if a major company were to go bankrupt?

Conclusion

In 2000, a member of my family took out a life insurance policy called "Euro-Emergence", a product marketed by the French Post Office. The "adviser's" first sales pitch was that it was a fund based on European equities, whose price would rise. Promise not kept. Second selling point: the capital gain would not be taxable after eight years. Present value of the investment: 40% of the initial investment, i.e. a loss of 60% of the capital. But rest assured, there is still enough capital left to deduct management fees each year...

If this person had invested in physical gold, the value of his investment would have risen from $300 an ounce in 2000 to $1,700 in 2012, a 460% increase in value. With no annual management fees (and possibly a modest storage fee). And totally exempt from capital gains tax on resale, since the ingot was held for 12 years (French tax code; other countries, including Switzerland, have no such tax).

Next article: 3° Investment funds, less efficient than a chimpanzee.

Author : La rédaction d’Euporos SA

Source : www.euporos.ch

Comments

No current comments